Energy Credits Expiring

New Tax Forms and updates, One Big Beautiful Bill updates (OBBB)

Online Payments to IRS only, No more paper checks!

Another year has passed, and tax season is upon us again. 2025 brought many changes to tax law. In this article, I will just briefly introduce the main items that will affect most taxpayers. One subject I will skip is payroll changes, because there are too many complex details to cover. (Hopefully the payroll company processed the W-2 correctly. If not, please make an appointment with me and we’ll try to straighten things out.) Please read each section carefully, because even the articles issued by the current administration can be misleading. Please note that tax rules are always changing, and I post this article with the most recent information available as of 1/3/26.

Energy Credits Expiring

All of the beloved energy credits expired in 2025. For electric vehicles, new and used, the tax credits expired on 9/30/25. All of the energy credits related to the home, for solar panels, energy efficient improvements on a home- they all expired on 12/31/25.

New Tax Forms and updates & OBBB

The IRS went all out this year and refreshed the entire 1040. The main theme is that the original postcard format has been changed into a more highly detailed version. Extra attention to detail has been applied to tax status for dependents showing the relationship to the taxpayer and filing status for Married Filing Separately (MFS), Qualified Surviving Spouse (QSS), and nonresident alien or dual status alien spouse.

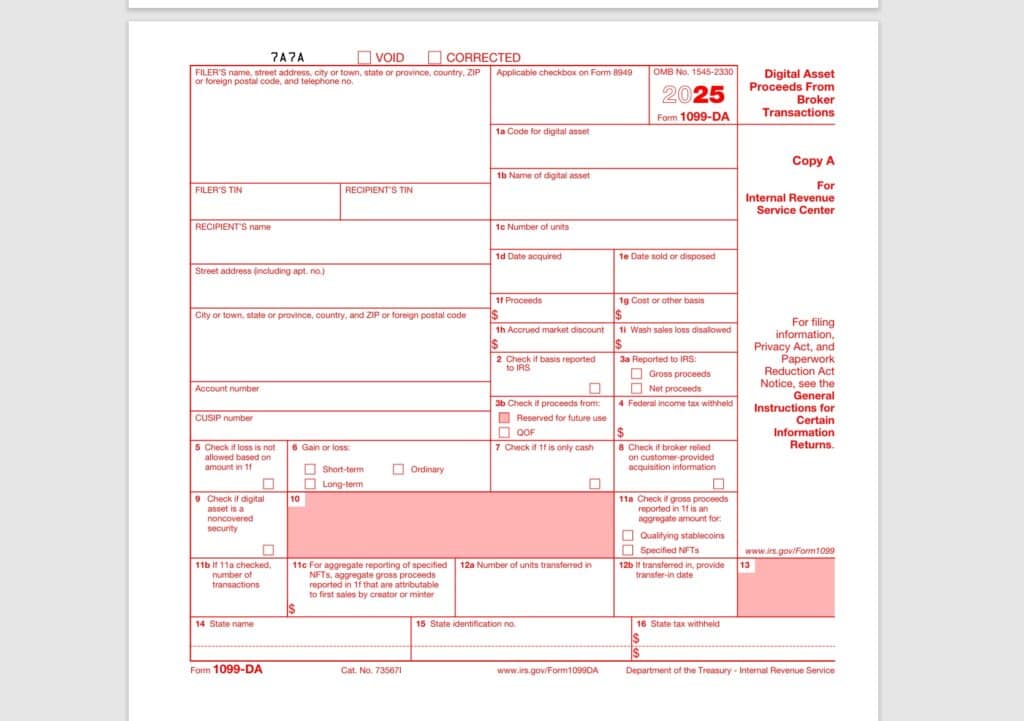

1099-DA

The 1099-DA is equivalent to the 1099-B. It is the tax form for reporting cryptocurrency transactions provided by the brokerage firm. “DA” stands for Digital Asset. IRS will enforce this on financial institutions to start reporting 1099-DA in 2026.

Student Loans

Employers can pay for student loans up to $5250, which is non-taxable. The $5250 amount will be adjusted for inflation starting in 2027. Student loans that are forgiven are generally taxable. Student loans can be forgiven/nontaxable if the taxpayer experiences death or disability.

Retirement Issues

Secure Act 2.0 finally addressed definition of disability for child versus an adult for the purposes of Social Security benefits.

For 2026, it’s probably a good idea to contribute more towards Roth if you qualify, since we anticipate future tax brackets to be higher in the future. (Please consult with your financial planner to make sure you qualify before contributing towards Roth.) For people aged 60-63, they can have additional catch up contribution of up to $11250.

For high earners who do qualified charitable donations (QCDS), starting 2025 there is a one time option to put up to 50% into Charitable Gift Annuity (CGA) or Charitable Remainder Trust (CRT).

If you’ve misplaced your retirement account, you can access the information here. You will need a login.gov account to access.

Salt Cap with *Phase Out*

With the current Trump administration, the SALT Tax has been adjusted up from $10k to $40k* per return. I put the asterisk there, because there’s a big caveat. The SALT cap eventually phases out to 30% when the tax return income hits $500k, but even high earners get at least $10k for SALT.

Miscellaneous Deductions at 2% permanently gone

All 2% deductions are gone. (State taxes do not mirror Federal return for 2025, so watch out!)

Disaster Loss Deductions

State declared disasters follow Federal rules for deducting losses. There’s nothing in the law about taking money from retirement to cover disaster loss. (Don’t do it!) And if you find yourself having to relocate due to a disaster, please remember to file change of address form with IRS: Form 8822.

“Nontaxable” Tip Income

I originally said I wouldn’t touch payroll issues in this article, but I felt that the public needs to know the truth about the details on “Nontaxable” Tip income. The devil is in the details. The nontaxable tips only apply to certain occupations that traditionally report tips. An example of someone who wouldn’t qualify for the “nontaxable tips” would be a musician. All of the tips the musician earned in 2025 would be taxable. To claim the nontaxable tips, there is an occupation code on Box 7 of the W-2. The tips collected would have to be from voluntary tips. An example of how a restaurant worker could get kicked out of nontaxable tips is if the restaurant did a mandatory tip for 6+ guests. Since the receipt automatically charged the tips, then that portion earned is fully taxable.

*No Tax* on Over Time

Ditto on the payroll comment. I felt strongly about spelling out the truth. There are many rules; it’s not as simple as it appears. The maximum deduction for individual is $12500, $25k for MFJ. MFS cannot claim No Tax on Overtime. The taxpayer doesn’t really get to claim all of the overtime pay, only the portion that exceed regular pay. Example: If you get paid $20/ hour and overtime pay is $30/ hour. You only get to claim $10/hour overtime pay exemption, up to $25k for MFJ tax return. The No Tax on Over Time phases out about 10% starting at $150k ($300K MFJ).

Car Interest Deduction for 2025 only

For 2025, if you purchased a new car assembled in the US, and started a car loan, you can deduct up to $10,000 on the car loan. There are some basic restrictions: not part of a fleet, not commercial, under 14,000 pounds, etc. MFS can claim this deduction. There is a phaseout subject to income levels at about 20%, starting at $100k ($200k for MFJ). To claim car interest deduction, you will need form 1099-VLI, and your car VIN. VIN information can be found here.

No Tax on Seniors (Mostly False)

The Social Security Administration issued a false statement on 7/3/24 to beneficiaries, claiming that, ” OBBB [includes a provision that eliminates federal income taxes on Social Security benefits for most beneficiaries]”. Social Security Administration has issued a correction notice as of 7/7/25.

Again, the devil is in the details. In addition to the traditional senior deduction of $2000 for single filers and $1600 for each qualifying spouse in a married couple, seniors can claim an additional deduction of $6000* for 2025. This additional senior deduction is subject to 6% phaseout starting at $75k ($150 MFJ). MFS cannot claim the extra senior deduction, and you must have a SS# to claim this additional deduction.

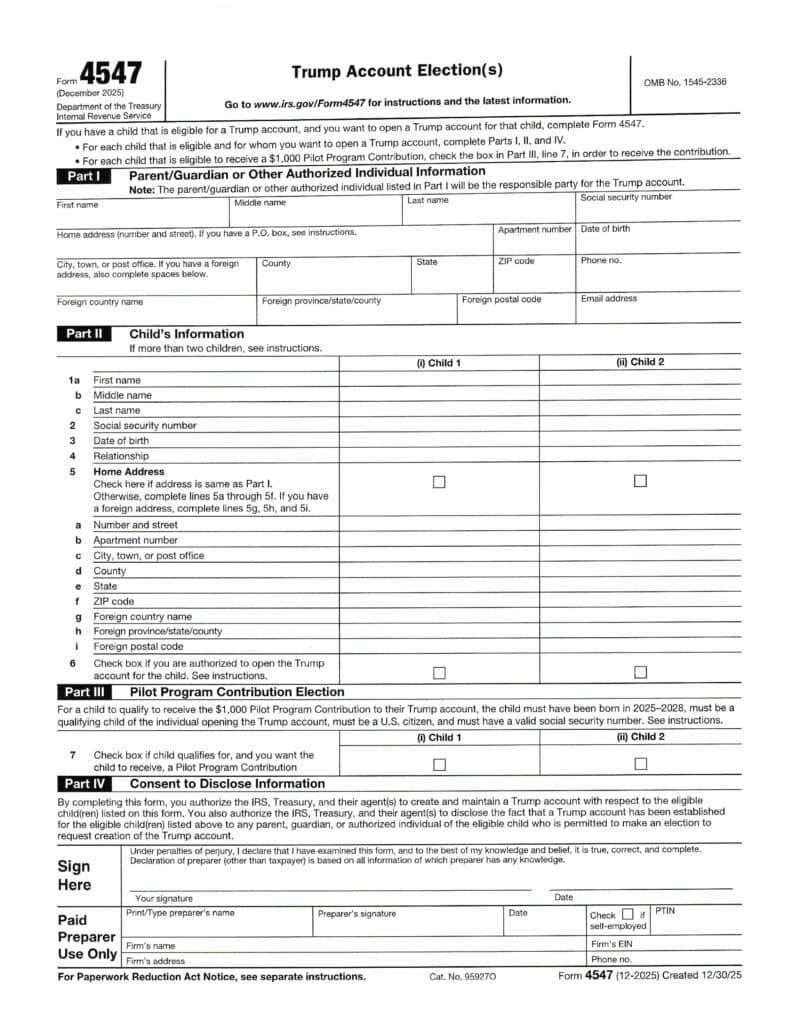

Trump Accounts

At first look, I thought it was a great deal getting free money for your kids. But it’s not that simple. If you have kids that are 14 years+, in my humble opinion, you’re probably better off investing in a 529 plan for college. Here are the hoops you need to jump through to get the free $1000 Trump money for your Trump Era kid. First off, the Trump account does not behave like a 529 plan. It behaves more like an IRA for your child. To receive the $1000, you must go online to trumpaccounts.gov and file form 4547 either with your tax return or separately. To my knowledge, you can’t apply for this until 7/5/26. (“4547” is to commemorate President Trump’s reign as POTUS.) The federal government will contribute $1000 for child with SS# born between 2024-2028. The caveat is that the child can’t touch the money until he or she turns 18 and only withdraw only 1/2 of the funds. The child has to turn age 26 to withdraw all of the money. It is not a $1000 government check; the money is put into a US Index Fund. (more details to come, see notice 2025-68) Up to $5000 of after tax money can be contributed annually by family members.

What originally drew me in is that employers of parent or child can contribute up to $2500, and non-profits can contribute to the Trump account. Right now, it’s unclear whether the contribution limits of the employers are annual or lifetime. My main concern is that the free $1000 Trump money can’t be touched until the child turns 18, and you have no real control over the investments.

No more Paper Checks

Per Executive order# 14247, IRS is no longer accepting paper checks. My personal suggestion is to make all of your tax payments on www.irs.gov/payments At least you can print out your tax payment receipts. I have fought this, because many seniors are visually challenged and struggle to read bank accounts on computer screens. Hopefully the government will realize this is a serious matter.